Reading an insurance policy document can feel confusing, especially if English is not your first language. Insurance documents are often full of technical words, small print, and many pages. But understanding your policy is important. It helps you know what is covered, what is not, and what to do if you need to make a claim.

This guide will help you read an insurance policy step by step. You will learn how to find important information, avoid mistakes, and feel confident about your coverage.

Why Reading Your Insurance Policy Matters

Many people only look at their insurance policy when there is a problem. This can lead to surprises. For example, you might think your car insurance covers theft, but find out later it does not. Or you may believe your health insurance pays for all hospital bills, but discover some limits.

Reading your policy in advance helps avoid these situations.

Insurance policies are legal contracts. You are agreeing to certain rules and conditions. If you do not know these details, you may lose money or benefits. A study by the National Association of Insurance Commissioners found that 33% of Americans do not fully understand their policies. Non-native English speakers face even greater challenges. Taking time to read and understand your policy can protect you from costly mistakes.

What Is An Insurance Policy Document?

An insurance policy document is a written contract between you and the insurance company. It describes:

- Who is covered

- What is covered

- What is not covered (exclusions)

- How much you pay (premium)

- How to make a claim

- The terms and conditions

Each policy is different. You may have policies for health insurance, auto insurance, life insurance, or property insurance. These documents often use similar parts and structure. Knowing how these parts fit together will make reading easier.

Credit: www.allstate.com

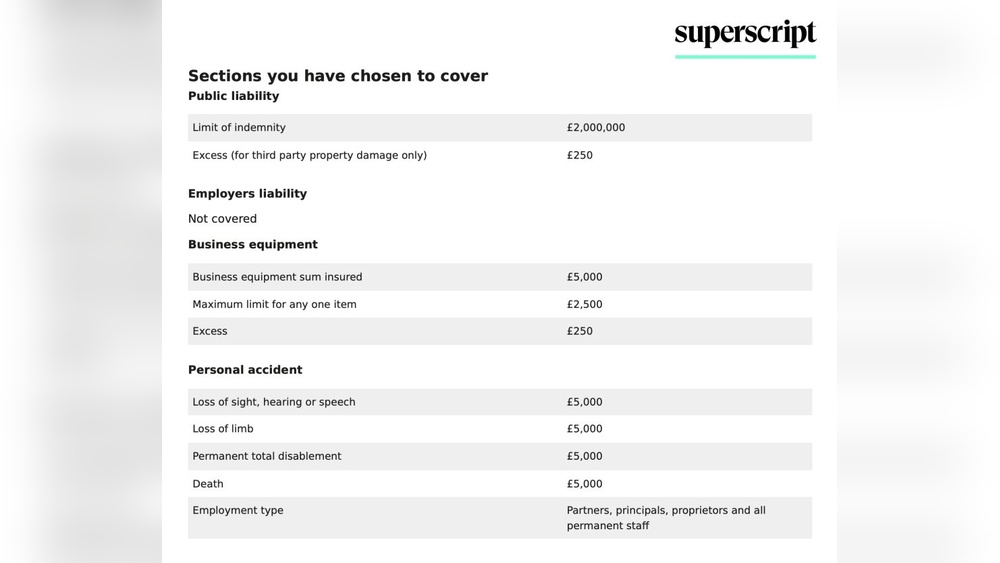

Key Sections Of An Insurance Policy

Most insurance policies follow a standard structure. Here are the main sections you will see:

| Section Name | Purpose |

|---|---|

| Declarations | Shows basic details: your name, policy number, coverage limits, premium |

| Definitions | Explains key terms used in the policy |

| Insuring Agreement | Describes what is covered and under what conditions |

| Exclusions | Lists what is NOT covered |

| Conditions | States your responsibilities and insurer’s responsibilities |

| Endorsements/Riders | Extra changes or additions to the standard policy |

Not all policies use the same words, but most have these basic sections. If you are reading a policy from another country, some parts may have different names.

Step-by-step: How To Read An Insurance Policy

Reading your policy is easier if you follow a process. Here is a step-by-step approach:

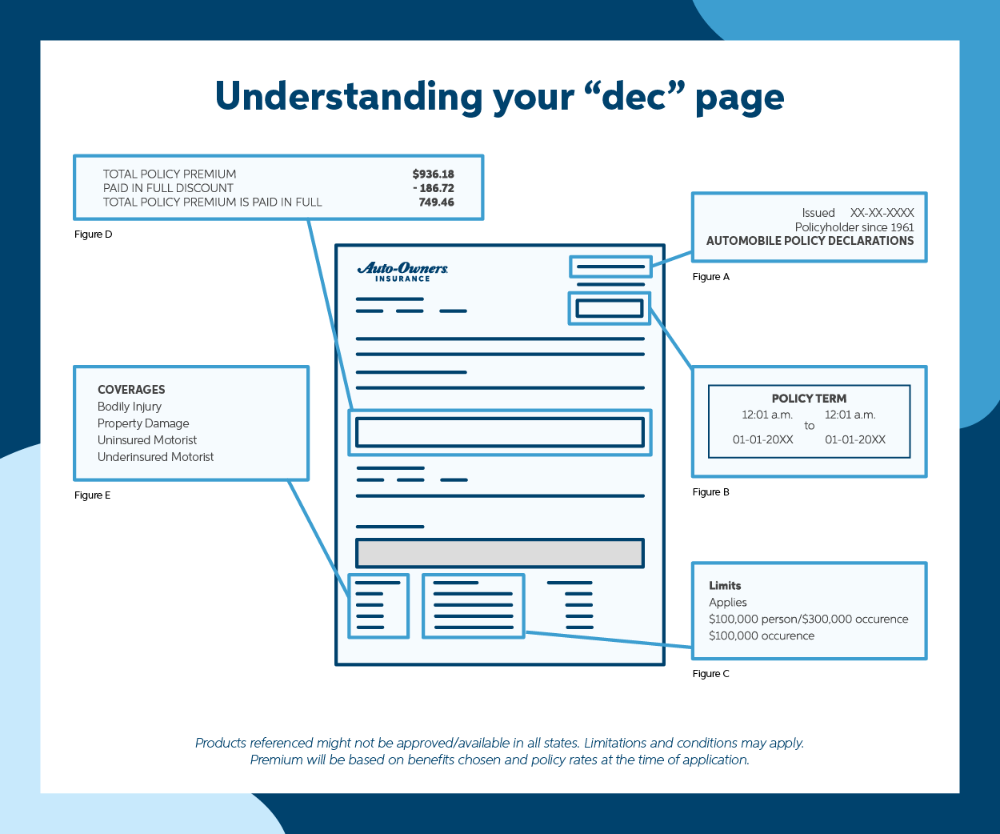

1. Start With The Declarations Page

This page is usually at the beginning. It shows:

- Policyholder name

- Policy number

- Start and end dates

- Covered items (like your car or house)

- Coverage limits (maximum amount insurer will pay)

- Premium (how much you pay)

Check that all details are correct. If anything is wrong, contact your insurer immediately.

2. Review Definitions

Insurance policies use special words. The Definitions section explains these. For example:

- Deductible: Amount you pay before insurance pays.

- Beneficiary: Person who gets benefits if you die.

- Peril: Cause of loss, like fire or theft.

Read this section carefully. Understanding these terms will help with the rest of the document.

3. Read The Insuring Agreement

This is the heart of your policy. It tells you:

- What is covered

- When coverage starts and ends

- How the coverage works

Look for phrases like “We will pay for…” or “Coverage includes…” This section shows what you can expect from your insurance.

4. Find The Exclusions

Many people skip this part. But exclusions are crucial. They list what is NOT covered. For example:

- Flood damage may be excluded in homeowners insurance.

- Cosmetic surgery may be excluded in health insurance.

If you see something you need (like flood coverage), ask your insurer about adding it.

5. Understand The Conditions

This section explains your duties. Common conditions include:

- Paying premiums on time

- Giving notice about changes (like moving house)

- Keeping records of losses or damages

If you break these rules, the insurer may refuse your claim. Read this part slowly and ask questions if needed.

6. Check Endorsements And Riders

These are extras added to your policy. They might increase coverage, remove exclusions, or change terms. For example:

- Adding jewelry coverage to home insurance

- Removing a driver from auto insurance

Always check these pages, especially if you requested changes when buying your policy.

Common Mistakes When Reading Insurance Policies

Many people misunderstand insurance documents because they:

- Skip the exclusions: They assume everything is covered.

- Ignore the definitions: Technical words can hide important limits.

- Forget to check endorsements: Changes may affect coverage.

- Miss renewal and cancellation terms: Policies may change each year.

- Overlook claim instructions: Not knowing how to file can delay payments.

Avoiding these mistakes will help you get the coverage you expect.

Comparing Insurance Coverage And Exclusions

Understanding differences between policies can help you choose the right one. Here’s an example comparing auto insurance coverage and exclusions:

| Feature | Basic Auto Insurance | Comprehensive Auto Insurance |

|---|---|---|

| Accident Damage | Covered | Covered |

| Theft | Not Covered | Covered |

| Flood Damage | Not Covered | Covered |

| Personal Injury | Limited | Better Coverage |

| Premium Cost | Lower | Higher |

This comparison shows why reading the exclusions and coverage is important. A basic policy costs less but covers fewer risks.

Practical Tips For Reading Insurance Policies

Reading an insurance policy is not just about checking boxes. Here are some practical tips:

- Take notes: Write questions or unclear points as you read.

- Use a highlighter: Mark key details, especially exclusions and claim steps.

- Ask for a summary: Many insurers offer simple summaries or “policy highlights.”

- Use translation tools: If English is difficult, use Google Translate or ask for a translated copy.

- Contact your agent: If something is not clear, ask for explanations or examples.

One non-obvious insight: policies often use “and/or” or “may” in conditions. These words can change coverage. For example, “may cover theft if…” means it is not guaranteed. Always check for these conditional phrases.

How To Handle Updates And Renewal Notices

Insurance policies change over time. Renewal notices may update coverage, premiums, or exclusions. Always read renewal documents carefully. If your policy changes, compare the new terms to your old policy. Look for:

- Higher premiums

- New exclusions

- Changes in coverage limits

If you do not agree with changes, contact your insurer before the renewal date. You may be able to negotiate or shop for a better policy.

Claim Filing: What To Look For In Your Policy

When you have a loss or accident, you need to file a claim. Your policy explains how to do this. Look for sections like “Claims” or “How to Report a Loss.” Common requirements include:

- Notifying the insurer quickly (often within 24–48 hours)

- Providing proof (photos, receipts, police report)

- Filling out claim forms

Missing deadlines or not giving enough proof can lead to denied claims. Some policies give step-by-step instructions. Others require you to call a helpline. Always check this section before you need it.

Here is a simple example of claim requirements:

| Policy Type | Notification Deadline | Proof Needed | Common Mistake |

|---|---|---|---|

| Auto Insurance | 48 hours | Photos, Police Report | Late reporting |

| Health Insurance | 30 days | Hospital Bills, Doctor Reports | Missing medical records |

| Home Insurance | 72 hours | Photos, Receipts | No proof of ownership |

Knowing these details in advance can help your claim go smoothly.

Non-obvious Insights For Beginners

- Look for hidden sub-limits: Some policies cover a total amount, but limit certain items. For example, you may have $50,000 in home coverage, but only $2,000 for jewelry.

- Understand ‘waiting periods’: Health and life insurance often have waiting periods before coverage starts. If you make a claim too soon, it may be denied.

Most beginners only check the big coverage numbers. But these smaller limits and waiting times can change what you get paid.

Credit: www.acceptance.com

Resources For Understanding Insurance Documents

If you need extra help, try these options:

- Ask your insurance agent for a policy summary

- Use online glossaries for insurance terms

- Check consumer guides from official sources like the National Association of Insurance Commissioners

- Find translated guides for your language

These tools can make reading policies easier and clearer.

Frequently Asked Questions

How Do I Know If Something Is Covered By My Insurance Policy?

Read the Insuring Agreement and Exclusions sections. If the item or event is listed in the agreement and not excluded, it is covered. If you are unsure, ask your insurer for confirmation.

What Should I Do If I Cannot Understand A Policy Term?

Check the Definitions section. If it is still unclear, look up the term online or ask your agent. Many official websites offer insurance glossaries.

Can I Request A Simpler Or Translated Version Of My Policy?

Yes. Most insurers can provide a plain-language summary or a translated version. If you need help, contact your agent or customer service.

What Happens If I Do Not Follow The Policy Conditions?

If you break a policy condition (like paying late or not reporting a claim), the insurer may deny your claim or cancel your policy. Always follow the rules stated in the Conditions section.

Are Policy Changes At Renewal Automatic?

Usually, insurers send a renewal notice with any changes. Read it carefully. If you do not agree with new terms, contact your insurer before the renewal date to discuss options.

Understanding your insurance policy is not just about reading—it is about knowing your rights and responsibilities. Take your time, ask questions, and make sure you have the coverage you need. With careful reading and attention to detail, you will avoid surprises and make better choices for your protection.

Credit: www.auto-owners.com

Read More:

- Reinsurance: What It Is and Why It Matters for Insurers

- Step-By-Step Guide to Filing an Insurance Claim: Expert Tips

- Understanding Risk And Insurance Pricing: A Simple Guide

- Digital Insurance (Insurtech) Trends in 2026: What to Expect

- AI and Automation in Insurance Industry: Transforming Claims Processing

- How to Switch Insurance Providers Without Losing Benefits Easily

- How Insurance Companies Make Money: Secrets Behind Their Profits

- What to Do After an Accident: Essential Insurance Checklist