Switching insurance providers can feel risky. Many people worry about losing benefits or facing gaps in coverage. But with careful planning, you can move to a new insurer smoothly—and sometimes, even improve your protection. This guide explains how to change insurance companies without sacrificing your current benefits. You’ll learn practical steps, mistakes to avoid, and how to compare providers. Whether you’re changing health, auto, or home insurance, the advice here will help you transition confidently.

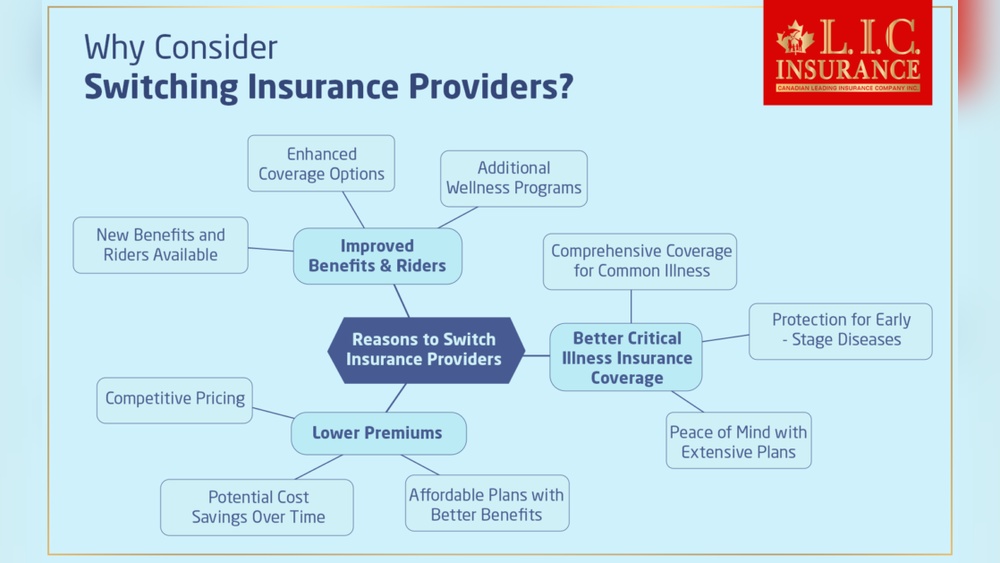

Why Switch Insurance Providers?

People switch insurance for many reasons. Maybe your premiums have gone up. Perhaps your current provider denies too many claims. Or you’ve found a company with better coverage for your needs. According to a 2023 survey by J.D. Power, about 30% of policyholders consider switching providers each year, mainly because of cost increases and poor customer service.

Switching can help you:

- Save money on premiums

- Get more suitable coverage

- Enjoy better customer service

- Access newer or more flexible policy options

But the main concern is keeping all your benefits. Let’s look at how to make the move without losing what matters.

Understand Your Current Policy

Before you switch, you need to know exactly what you have. Many people skip this step and later regret it.

- Review your policy documents. Look for details about coverage limits, deductibles, exclusions, and special benefits.

- Check renewal dates and cancellation terms. Some policies charge fees if you leave before renewal.

- List the benefits you value most, such as accident forgiveness, free annual health checks, or flood coverage.

Here’s a comparison of common features in home insurance policies:

| Feature | Standard Policy | Premium Policy |

|---|---|---|

| Water damage | Limited | Full |

| Personal property | Up to $10,000 | Up to $50,000 |

| Accidental damage | Excluded | Included |

| Flood coverage | Optional | Included |

Comparing your current benefits will help you demand similar—or better—coverage from your new provider.

Research New Providers Carefully

Not all insurance companies offer the same benefits. Some are cheaper but cut corners on coverage. Others may seem better but have hidden exclusions.

Key Factors To Compare

- Coverage types and limits

- Premium costs

- Customer service ratings

- Claim settlement speed

- Extra perks (roadside assistance, free health check-ups, etc.)

A 2022 study by the National Association of Insurance Commissioners found that companies with high customer satisfaction often resolve claims 20% faster.

Here’s a simple table comparing two auto insurance providers:

| Provider | Annual Premium | Claim Response Time | Accident Forgiveness |

|---|---|---|---|

| Alpha Insurance | $1,200 | 48 hours | Yes |

| Beta Assurance | $1,050 | 72 hours | No |

Always check reviews and ratings on independent sites. For health insurance, compare the network of hospitals and doctors. For auto, look for coverage extras like rental car reimbursement.

Non-obvious Insight

Some new policies may include waiting periods for certain benefits, especially for health or life insurance. This is a detail most beginners miss, so always ask about waiting periods for benefits before you switch.

Plan The Timing Of Your Switch

Timing is crucial. If you cancel your old policy before the new one starts, you might have a coverage gap. This can be risky—and in some cases, illegal (like driving without insurance).

- Overlap your policies by a few days. This ensures you’re always covered.

- Avoid switching during claim processing. If you have an open claim, resolve it first.

- Choose renewal periods for switching, when possible. This avoids penalties and missed benefits.

Steps To Switch Without Losing Benefits

Follow this checklist to make your switch smooth:

- Identify must-have benefits from your current policy.

- Get quotes from at least three providers. Request clear benefit lists.

- Compare policies line-by-line. Use a comparison table if helpful.

- Ask questions about waiting periods, exclusions, and add-ons.

- Check for transfer options. Some benefits (like no-claim bonuses) can be transferred.

- Apply for the new policy but do not cancel your old one yet.

- Wait for approval from the new provider. Make sure all benefits are confirmed.

- Cancel your old policy only after your new policy is active.

- Keep documentation from both providers.

Common Mistakes To Avoid

- Canceling your old policy before your new one starts

- Not checking for waiting periods or exclusions

- Missing out on transferable benefits (like accident forgiveness or no-claim bonuses)

- Overlooking cancellation fees or refund policies

Handling Transferable Benefits

Some benefits can move with you. For example, no-claim bonuses in auto insurance reward you for safe driving. Many insurers let you transfer this to your new policy.

How To Transfer

- Request a no-claim bonus certificate from your old provider.

- Share it with your new insurer.

- Confirm the bonus is applied before you pay for the new policy.

Some health insurance companies allow you to transfer waiting periods or portability benefits if you switch to a similar plan. Always ask about this.

Credit: www.helloglobo.com

Dealing With Pre-existing Conditions

For health insurance, pre-existing conditions can cause trouble. Some providers refuse coverage, or require waiting periods.

Key tips:

- Choose a provider with a strong network of hospitals.

- Ask about coverage for chronic illnesses.

- Check if your waiting periods for pre-existing conditions can be transferred.

If you’re switching for better coverage, make sure your new plan actually improves your situation.

Document Everything

Keep records of:

- Your old policy documents

- Cancellation letters or emails

- New policy confirmations

- Any certificates (like no-claim bonus)

This prevents confusion if you need to make a claim or prove coverage history. Many insurers may ask for proof, especially when transferring benefits.

Credit: www.knightinsurance.com

Practical Example: Switching Auto Insurance

Let’s say you have auto insurance with Provider A. Your premium is rising, and you want better accident coverage. You compare quotes from three providers, focusing on accident forgiveness and roadside assistance.

You discover Provider B offers similar premiums but adds free towing and accident forgiveness. You apply for the new policy. Once it’s active, you cancel Provider A’s policy, making sure your no-claim bonus is transferred.

By overlapping policies and confirming transferable benefits, you avoid losing accident forgiveness—a benefit many drivers value.

Negotiating With New Providers

When you switch, you have bargaining power. Insurers want your business, especially if you have a clean claim history. Use your no-claim bonus or your history of safe driving to ask for discounts.

If you’re moving health insurance, ask for coverage matching—some providers will match or improve your old benefits to win your business.

.jpg)

Credit: www.grangeinsurance.com

How To Compare Policies: Quick Checklist

- Coverage types and limits

- Premiums and deductibles

- Special benefits and add-ons

- Waiting periods and exclusions

- Customer reviews and claim settlement times

- Transferable benefits

Data: How Many People Switch Without Losing Benefits?

According to a 2023 Insurance Consumer Report, about 65% of people who switch insurance providers retain all key benefits if they follow proper steps. Those who skip comparing policies or forget about waiting periods often lose important coverage.

When Should You Not Switch?

Switching isn’t always the best option. If you have an open claim, or if your new provider doesn’t match your must-have benefits, it’s better to wait.

Also, if you’re in the middle of a policy period and cancellation fees are high, wait until renewal. Sometimes, loyalty discounts or long-term perks can outweigh the benefits of switching.

Special Tips For Non-native English Speakers

Insurance language can be confusing. Ask for policy documents in simple English if possible. Use translation tools to understand details. Many insurers offer customer support in multiple languages. Never sign a new policy unless you understand all terms.

Useful External Resource

For more detailed guidance on switching health insurance, visit Healthcare.gov.

Frequently Asked Questions

What Happens If There Is A Gap Between My Old And New Insurance Policies?

A gap can leave you unprotected. For auto insurance, you may face fines or legal trouble. For health or home insurance, you risk paying out-of-pocket for accidents or emergencies. Always overlap policies by a few days.

Can I Transfer My No-claim Bonus To A New Provider?

Yes. Most auto insurers allow you to transfer your no-claim bonus. Ask your old provider for a certificate and share it with your new insurer.

Are There Fees For Canceling An Insurance Policy Early?

Many providers charge cancellation fees or reduce refunds if you cancel before renewal. Check your policy terms before switching.

What Should I Do If My New Provider Denies Coverage For A Pre-existing Condition?

Look for insurers that accept pre-existing conditions or offer portability benefits. Compare waiting periods and exclusions before you switch.

How Can I Be Sure My New Policy Includes All The Benefits I Need?

Ask for a detailed benefit list in writing. Compare it to your current policy. If possible, use a comparison table to check coverage side by side.

Switching insurance providers can be straightforward if you plan ahead. By carefully comparing policies, timing your switch, and transferring key benefits, you protect yourself from losing important coverage. Always read the fine print, ask questions, and keep records. With these steps, you can confidently change insurance companies and enjoy the best protection for your needs.

Read More:

- Reinsurance: What It Is and Why It Matters for Insurers

- Step-By-Step Guide to Filing an Insurance Claim: Expert Tips

- Understanding Risk And Insurance Pricing: A Simple Guide

- Digital Insurance (Insurtech) Trends in 2026: What to Expect

- AI and Automation in Insurance Industry: Transforming Claims Processing

- How to Read an Insurance Policy Document: A Simple Guide

- How Insurance Companies Make Money: Secrets Behind Their Profits

- What to Do After an Accident: Essential Insurance Checklist