No one expects to be in an accident, but it happens every day. If it happens to you, staying calm and knowing what to do can make a big difference. You must protect yourself, help others if needed, and handle your insurance correctly.

Many people forget important steps because they feel stressed or confused. Missing a single detail can lead to delays, denied claims, or extra costs. Here’s a practical guide to help you manage the situation and your insurance checklist after an accident.

This advice is easy to follow, even if English is not your first language.

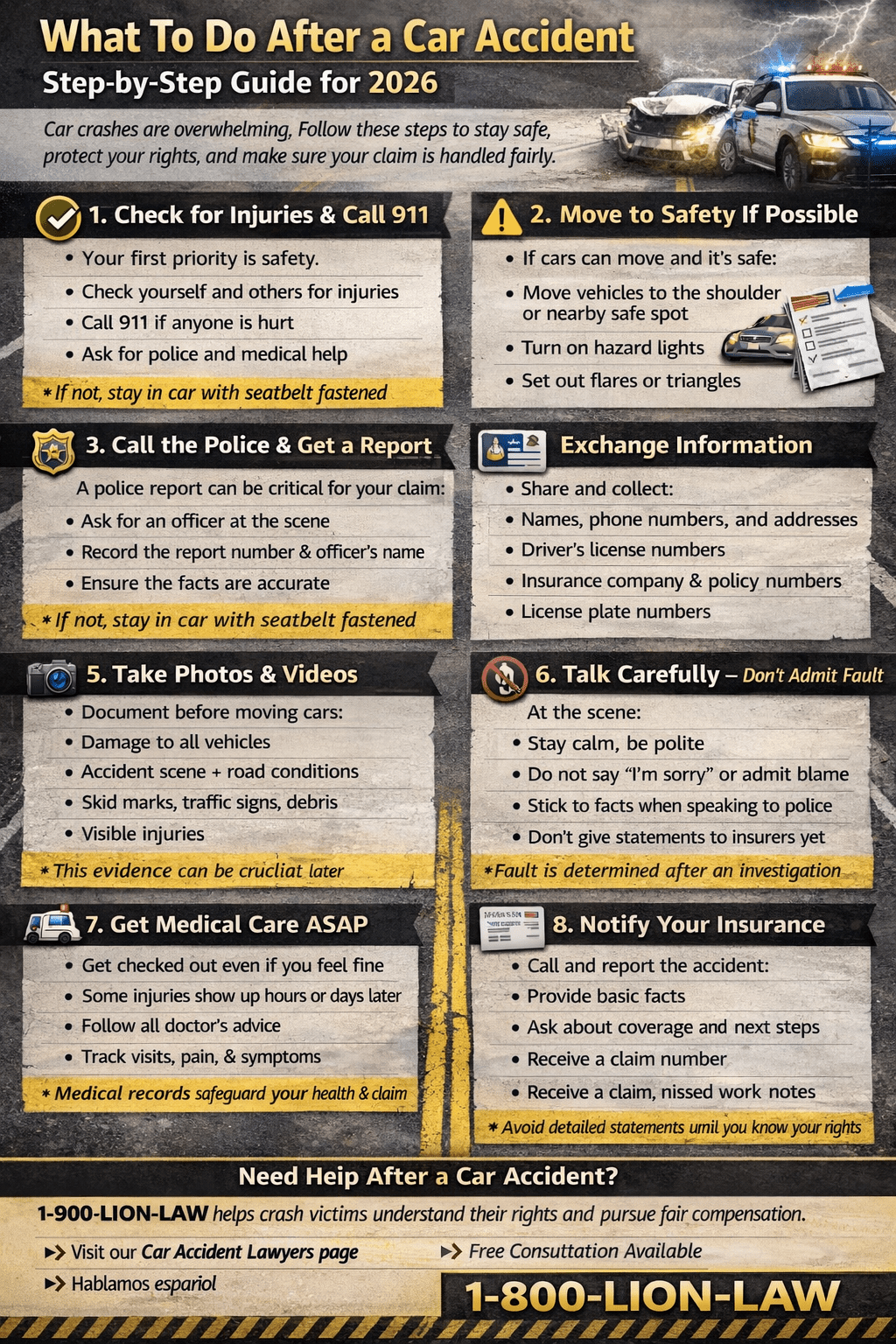

Stay Safe And Assess The Situation

Your first action after an accident is to check for injuries. If anyone is hurt, call 911 immediately. Do not move injured people unless it’s dangerous to leave them where they are, like in the middle of a busy road. If the vehicles are safe to move, pull over to a secure spot.

Turn on your hazard lights to warn other drivers. If it’s dark, use a flashlight or phone to make yourself visible. Check for leaking fluids, smoke, or fire. If you notice these, move away quickly.

It’s normal to feel shocked or upset. Take a few deep breaths before you speak to anyone. This helps you think clearly and avoid saying something you might regret later.

Gather Essential Information

Accidents can be confusing, but collecting the right details is crucial. Insurance companies need accurate information to process your claim. Here’s what you should gather:

- Names and contact information of all drivers and passengers

- License plate numbers

- Driver’s license numbers

- Vehicle make, model, and color

- Insurance details for each driver (company name, policy number)

- Location of accident (street name, nearest intersection)

- Time and date

- Weather conditions (rain, fog, clear)

Take photos of everything: vehicles, damage, street signs, and injuries if any. Snap pictures from different angles. If there are witnesses, ask for their names and phone numbers.

Don’t rely only on your memory. Write everything down or use your phone’s notes app. Details can be forgotten quickly, especially in stressful moments.

Notify The Police And File A Report

In most states, you must report accidents involving injuries, property damage, or if the other driver leaves the scene. Even if the crash seems minor, it’s wise to call the police.

When officers arrive, give them clear, honest answers. Do not guess or speculate. Ask for the police report number and the officer’s name. This report will help your insurance claim and may be required by law.

If police do not come (for example, in a small fender bender), you can often file a report online or at the local station. Keep a copy for your records.

Contact Your Insurance Company

Notify your insurance provider as soon as possible. Most companies have a 24-hour hotline. Delaying your report can cause problems with your claim.

Prepare these details before calling:

- Your policy number

- Accident location and time

- Names of involved parties

- Description of damage

- Police report number (if available)

- Photos of the scene and damage

Describe the accident truthfully, but stick to the facts. Avoid blaming yourself or others. Your insurance adjuster will investigate and determine fault.

Some companies offer apps for reporting accidents. These can speed up the process, but always keep a backup record.

Insurance Checklist: What To Submit

Here’s a step-by-step checklist for your insurance claim:

- Accident report (police or self-report)

- Photos of vehicles and scene

- Contact information for all involved

- Insurance details from other driver(s)

- Repair estimates (if possible)

- Medical bills (if injured)

- Witness statements

Ask your insurer if they need anything else. Missing documents can delay your claim. If you’re unsure, send more information rather than less.

Understanding Fault And Coverage

Insurance companies look at the facts to decide who caused the accident. Sometimes, both drivers share blame. In the US, rules differ by state. Some states use “no-fault,” meaning your own insurance pays for your injuries, no matter who caused the crash.

Here’s a simple comparison of fault systems:

| System | Who Pays | Typical States |

|---|---|---|

| At-fault | Driver responsible for accident | Texas, California |

| No-fault | Your own insurance | Florida, New York |

Your policy may cover liability, collision, or comprehensive damage. Review your coverage before an accident, so you know what to expect. If you don’t understand a term, ask your agent for help.

Repairing Your Vehicle

After your claim is filed, your insurance may recommend repair shops. You can choose your own, but using a preferred shop can speed up approval.

Ask for a written estimate before work begins. Compare estimates from two or three shops if possible. Some shops charge more for the same repair.

Here’s an example of how costs can differ:

| Repair Shop | Estimated Cost | Warranty Offered |

|---|---|---|

| Shop A | $1,200 | 1 year |

| Shop B | $1,000 | 6 months |

| Shop C | $1,450 | 2 years |

Keep all receipts and paperwork. Your insurance may need them to reimburse you.

Medical Treatment And Documentation

Even if you feel fine, see a doctor after an accident. Some injuries appear days later. Your insurance may cover medical bills if you report them quickly.

Tell your doctor about the accident and ask for a written report. Save copies of all bills, prescriptions, and treatment records.

Common mistake: Many people wait too long to see a doctor, thinking they’ll recover on their own. This can lead to denied claims or worsening health.

Credit: 1800lionlaw.com

Following Up And Handling Disputes

After you submit your claim, keep track of its status. Ask your adjuster for updates every week. If you disagree with the insurance decision, you have options:

- Request a review or appeal

- Provide more documents or photos

- Speak to a supervisor

If you feel your claim was unfairly denied, you can file a complaint with your state insurance department. Some states have free mediation services to resolve disputes.

Non-obvious Insights For Accident Claims

- Check your policy for rental car coverage. If your car is being repaired, your insurance may pay for a temporary vehicle. Many drivers don’t realize this benefit exists.

- Keep a personal accident diary. Write down how you feel each day, any pain, or trouble at work. This record can help with medical or lost wage claims later.

- Don’t post accident details on social media. Insurance companies sometimes check Facebook or Instagram for conflicting statements.

- Notify your employer if the accident affects your ability to work. Your insurer may require proof of lost wages.

- Review your insurance renewal after an accident. Rates may rise, but you may qualify for discounts or better coverage.

Credit: www.enjuris.com

Common Mistakes To Avoid

- Leaving the scene without exchanging information

- Admitting fault before the facts are clear

- Forgetting to file a police report when required

- Waiting too long to contact your insurance

- Not documenting injuries or damage with photos

- Ignoring paperwork or missing deadlines

- Not following up on the claim’s progress

Example Case: Minor Accident

Let’s look at a real-life scenario. Maria was rear-ended at a stoplight. She felt fine but noticed neck pain later. She took photos, called the police, and exchanged information. She notified her insurer and saw a doctor the next day.

Maria submitted all documents and kept a diary of her symptoms. Her claim was approved, and her medical bills were covered. By staying organized and acting quickly, Maria avoided common mistakes.

Credit: hlalawfirm.com

Useful Resources

For more details about accident reporting laws and insurance, see the official USA.gov Insurance Guide. This site explains coverage types, claims, and state rules in simple language.

Frequently Asked Questions

What Should I Do If The Other Driver Does Not Have Insurance?

If the other driver is uninsured, your policy may cover you if you have uninsured motorist coverage. Call your insurer and explain the situation. You may need extra documents, but your company will guide you.

How Long Do I Have To Report An Accident To My Insurance?

Most insurers require you to report within 24–72 hours. Check your policy for exact deadlines. Delayed reporting can lead to denied claims.

Will My Insurance Rates Go Up After An Accident?

If you are at fault, your rates may increase. If you have accident forgiveness, your first accident may not affect your rates. It depends on your company and state rules.

What If I Disagree With The Insurance Company’s Decision?

You can request a review, provide more evidence, or file an appeal. If you still disagree, contact your state insurance department or use mediation services.

Do I Need A Lawyer After An Accident?

Usually, you don’t need a lawyer for simple claims. For serious injuries, disputes, or large damages, legal advice can help protect your rights.

Handling an accident is never easy, but following these steps can make things smoother. Stay calm, gather details, and work closely with your insurance. Protect yourself and your rights by being organized and proactive. Remember, mistakes can cost time and money, but preparation pays off.

Read More:

- Reinsurance: What It Is and Why It Matters for Insurers

- Step-By-Step Guide to Filing an Insurance Claim: Expert Tips

- Understanding Risk And Insurance Pricing: A Simple Guide

- Digital Insurance (Insurtech) Trends in 2026: What to Expect

- AI and Automation in Insurance Industry: Transforming Claims Processing

- How to Read an Insurance Policy Document: A Simple Guide

- How to Switch Insurance Providers Without Losing Benefits Easily

- How Insurance Companies Make Money: Secrets Behind Their Profits